The news, bloggers, social media, everyone is talking about the looming interest rate and bond crisis. They mention the war in Iran, price inflation, oil shocks, and even mystery sellers who are allegedly dumping U.S. Treasuries. While they’re not wrong, since these influence rates, there is a massive component completely missing from the mainstream narrative. Let’s unmask this using our causal-realist approach.

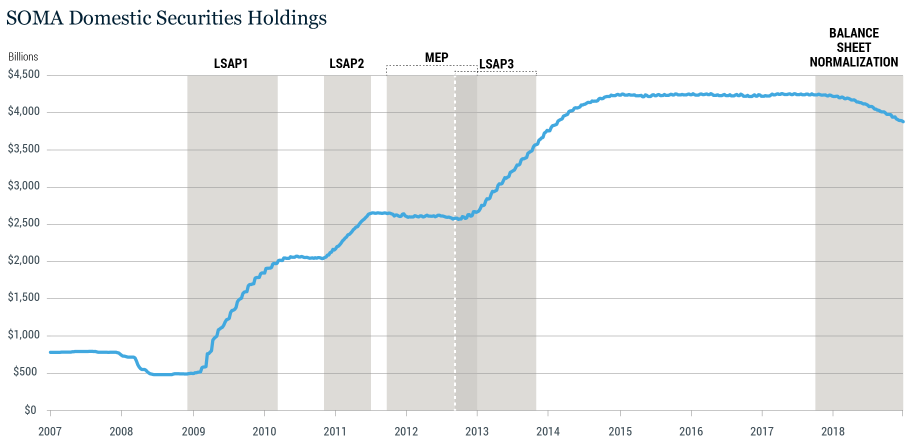

Courtesy of the NY Fed (italics added for emphasis):

First Round of (LSAP) Large-Scale Asset Purchases (2008-2010) – QE1

From November 2008 to March 2010, the first round of large-scale asset purchases included purchases of $175 billion in agency debt, $1.25 trillion in agency MBS, and $300 billion in longer-term Treasury securities.

Second Round of (LSAP) Large-Scale Asset Purchases (2010-2011) – QE2

From November 2010 to June 2011, the second round of large-scale asset purchases included $600 billion in longer-term Treasury securities.

Maturity Extension Program (2011-2012) – Operation Twist

From September 2011 through 2012, the Maturity Extension Program, commonly known as Operation Twist, included purchases of $667 billion in Treasury securities with remaining maturities of 6 years to 30 years, offset by sales of $634 billion in Treasury securities with remaining maturities of 3 years or less…

Third Round of (LSAP) Large-Scale Asset Purchases (2012-2014) – QE3

… also included monthly purchases of $45 billion in longer-term Treasury securities, dropping to monthly purchases of $40 billion in January 2014 and decreasing by $5 billion after each FOMC meeting until October 2014. In total, the Federal Reserve purchased $790 billion in Treasury securities and $823 billion in agency MBS in the third purchase program.

Balance Sheet Normalization – QT

Starting in October 2017, the FOMC began to reduce its securities holdings to normalize the size of its balance sheet…

The balance sheet didn’t substantially begin to shrink until about mid-2018. The Fed continued to tighten until the recession and COVID-crash (Austrian business cycle theory tells us the tightening induces the crash put in motion by the original expansion, but everything else gets the blame).

Each iteration of Quantitative Easing (QE) exemplified the Austrian nightmare: the suppression of interest rates. By manipulating the long end of the yield curve, the Fed severely distorted the structure of production. Especially when long-term rates are artificially suppressed, capital projects requiring years to manifest suddenly appear highly profitable to the private sector, while government pet projects look cheap and pork-barrel spending becomes all the more enticing.

It’s bad enough to suppress any rate, even the short end, but when the long end is suppressed, every long-term project looks good. This distortion of the pricing mechanism is the ultimate driver of widespread malinvestment.

Here we are today, which started on December 10, 2025, when the FOMC issued a new directive to the Open Market Trading Desk:

...to maintain an ample level of reserves through purchases of Treasury bills and, if needed, other Treasury securities with remaining maturities of 3 years or less. Additionally… to continue to reinvest all principal payments received from the Federal Reserve’s holdings of agency securities into Treasury bills.

And there you have it. QE involved the expansion of the money supply (i.e., monetary inflation) but it also suppressed long-term rates for a very long time.

While the Fed’s balance sheet is expanding once again ($178 billion since the inception of this policy), it can be confused for QE. However, consider the contrast:

- Purchase of Mortgage-Backed Securities (MBS)? Under QE, yes. Under RMP, no. If looking solely at the MBS balance, it’s undergoing the most seamless QT we’ve ever seen… for now.

- Purchase of Long-Term Treasuries? Under QE, yes. Under RMP, yes, “but” the Fed is explicitly restricting its purchases to short-term Treasury bills.

By refusing to buy long-dated bonds, the Fed is doing something unprecedented in the modern interventionist era, leaving long-term interest rates to be determined by the market.

If QE was the economic system on steroids, RMP is an IV drip designed to keep whatever is left of the economy, even if in name only, alive. RMP is not QE, nor is it QT. It’s just another made-up, unsound policy; and shameful because it’s not economics.

Should you apply truth, logic, and deductive reasoning to form a normative view, you’ll find that all intervention in the market is bad and the reason why we don’t have a true “free market.” This will be no different. We’re truly in uncharted waters, and so far it’s not looking good, but it will most assuredly get worse.